It’s 2026 – the cyber insurance industry can no longer attribute volatility to market immaturity alone. After more than a decade of live claims experience, repeated loss cycles, and increasingly sophisticated attacks, the industry’s most persistent challenge is no longer whether cyber risk can be insured, but how risk intelligence flows, or fails to flow, across the ecosystem.

At the center of this challenge sits a structural problem: cyber insurance data silos. Actuarial, underwriting, claims, and incident response (IR) functions continue to operate in largely sequential, disconnected loops. Each group performs its role competently in isolation, yet the system as a whole underperforms. The cost of this fragmentation is now visible in sustained loss ratio pressure, mispriced risk, and a widening gap between technical reality and insurance outcomes.

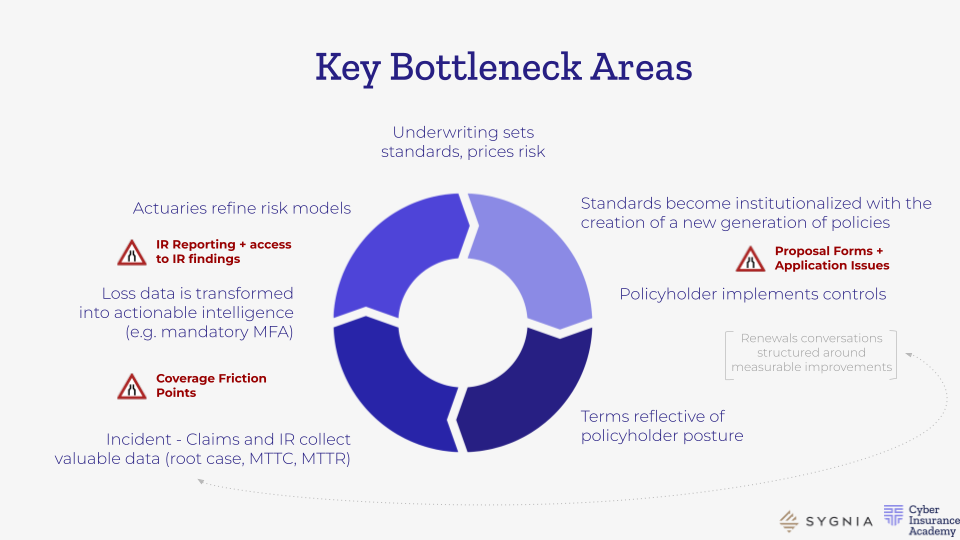

Where the System Breaks: Key Bottlenecks Across the Cyber Insurance Lifecycle

The future of cyber underwriting will be defined by whether the industry can move beyond this siloed model toward Integrated Cyber Risk Management: a collaboration framework where claims, IR, and underwriting continuously inform one another in near real time.

1. Actuaries Refine Risk Models With Incomplete Inputs

Cyber is still relatively new compared to property or marine, and actuarial teams are still working with limited historical loss data. To compensate, actuaries increasingly rely on third-party vendors, external modeling tools, and selected IR datasets. Yet these inputs are often inconsistent, incomplete, or abstracted away from real-world attack mechanics.

Integrating detailed IR findings, particularly those involving novel attack vectors or advanced threat actor behavior, into actuarial models is complex and slow. The result is a structural lag between how cyber risk manifests and how it is modeled.

Impact:

Ellisa Doroff shares in her masterclass, Lessons from Loss, “When exposure is under- or overestimated, pricing accuracy suffers.” These distortions cascade downstream, influencing underwriting appetite, policy wording, and even the security controls insurers emphasize.

2. Underwriting Sets Standards and Prices Risk Under Pressure

Underwriters are forced to make high-stakes decisions using application data that is often incomplete, misunderstood, or inconsistently validated. Even where intent is good, questionnaires remain a blunt instrument for capturing nuanced cyber risk. In competitive markets, pricing pressure further compounds the issue. Premiums may be driven as much by market dynamics as by technical exposure, decoupling risk selection from actual loss potential.

Impact:

Poor data quality erodes underwriting confidence and increases volatility. Risk may be priced too conservatively, constraining growth, or too leniently, amplifying loss ratios. Over time, this mispricing distorts how buyers perceive the value of cyber insurance itself.

41% of insurance decision-makers identify poor data quality as the primary obstacle to robust decision-making, while 36% cite a lack of collaboration between departments as a direct driver of operational cost. Underwriters spend significant time “chasing” claims data or manually correlating forensic IR reports with policy applications because internal systems often do not communicate effectively. This fragmented workflow slows decision-making, increases the risk of mispricing, and reinforces operational silos, undermining both portfolio performance and client confidence.

3. Standards Become Institutionalized Too Slowly

Translating actuarial insights and IR intelligence into formal policy language is a slow, consensus-driven process. By the time emerging threats are reflected in standardized clauses, attackers have often moved on. This institutional lag creates rigidity. Policies risk being anchored to yesterday’s threat models, while underwriting decisions attempt to anticipate tomorrow’s losses.

The implications extend beyond primary insurers. Limited information sharing between insurers and reinsurers leads to lower overall market capacity and higher premiums (Journal of Cybersecurity). Reinsurers often act as “information clearinghouses” but, in the absence of real-time data, are forced to price for the worst-case asymmetry. As a result, reinsurers are increasingly cautious of “blind” portfolios. If a primary insurer cannot demonstrate a current, aggregated view of risk, reinsurers may impose higher premiums or restrict capacity to cover that uncertainty.

Impact:

Coverage may fail to reflect the current risk environment, leaving insurers exposed and policyholders unclear on how their real-world security posture affects coverage or claims outcomes.

4. Policyholders Implement Controls In the Dark

Third-party assessments are often perceived by insureds as punitive rather than collaborative. Cooperation may be partial, and many assessments represent only a snapshot in time, failing to capture continuous improvement or adaptive controls. Critically, control data is rarely integrated back into underwriting in a way that meaningfully influences terms or pricing.

Impact:

Insurers operate with an incomplete understanding of policyholder posture, while policyholders miss opportunities to receive targeted guidance that could materially reduce loss exposure.

5. Terms Reflect Posture, But Not Dynamically

Policy terms are typically static across the policy period, even as security controls evolve. Feedback loops from claims and IR back into underwriting remain limited, restricting the ability to adjust terms based on real-world performance.

Impact:

Misalignment between actual posture and contractual terms can trigger disputes during claims or unnecessary friction. Trust erodes on both sides, undermining the insurer-insured relationship.

6. When Incidents Occur, Data Is Collected Slowly and Inconsistently

Elissa explains, “When incidents happen, claims and IR teams collect invaluable data: root cause, mean time to contain (MTTC), mean time to remediate (MTTR), and control failures.” Yet collection processes vary widely, reporting may be incomplete, and disclosure is often constrained.

Impact:

Delayed or inconsistent incident data limits the ability to refine models, adjust underwriting standards, or update policy language. The industry repeatedly relearns the same lessons.

7. Loss Data Becomes Intelligence

Transforming raw incident data into actionable intelligence requires coordination across actuarial, underwriting, IR, and brokers. Organizational silos and confidentiality concerns frequently block this translation.

Impact:

Without actionable intelligence, insurers cannot continuously improve pricing or guidance. Policyholders remain exposed to repeat events, and systemic resilience stagnates.

The Cost of the Claims Data Gap

At the heart of these bottlenecks lies the claims data gap, which stems from the failure to extract, structure, and share technical insights in a way that informs underwriting and actuarial decisions.

The cost is profound:

- Market sustainability suffers: Inefficient risk transfer restricts reinsurance participation, increases premiums, and limits market capacity.

- Risk modeling accuracy declines: Early pricing models were described by some executives as a “complete guess,” contributing to loss ratios exceeding 130% during the ransomware surge.

- Knowledge is squandered: Forensic insights are often buried behind privilege, preventing insurers from identifying which controls, such as MFA, truly reduce loss.

- Societal benefit erodes: While the economic cost of cybercrime has been estimated between $57–$109 billion, insurance payouts have represented less than 1% in some years.

- Actuarial fairness breaks down: Premiums become noisy, discouraging participation and reducing trust in the risk-transfer mechanism.

As Elissa notes, “The industry is currently in an ‘Actuarial Groundhog Day’ – we are pricing tomorrow’s volatility using the redacted footprints of yesterday’s failures.”

Proactive Cyber Underwriting: Necessary, But Not Sufficient

Proactive cyber underwriting offers a partial solution. By leveraging internal telemetry through read-only APIs and security partnerships, insurers gain real-time visibility into control performance rather than relying solely on annual questionnaires.

The upside is real:

- More accurate, objective risk assessment

- Earlier detection of exploitable vulnerabilities

- Streamlined applications and premium incentives for strong security

But challenges remain. Telemetry raises privacy concerns, requires deep technical expertise, and struggles to assess softer risk dimensions like governance and culture. Proactive underwriting improves inputs, but without integrated collaboration across claims, IR, and underwriting, it cannot fix the system alone.

The 2026 Imperative: Integrated Cyber Risk Management

The future of cyber underwriting will not be defined by better tools in isolation, but by integration. Claims, IR, and underwriting must operate as a continuous intelligence loop sharing data, aligning incentives, and translating technical reality into insurable insight. Integrated Cyber Risk Management is the minimum viable operating model for a market that wants to remain solvent, credible, and relevant in 2026 and beyond. The cost of maintaining silos is now measurable. The cost of changing them is strategic and unavoidable.