Cyber Insurance policies may look increasingly similar on paper, but the outcomes are not, and the gap between a commercialized cyber insurance carrier and a high-performance one is widening fast. However, this gap only becomes apparent once a real incident occurs.

Just as a great cyber insurance broker elevates outcomes for clients, a great cyber carrier elevates outcomes for policies. The difference lies in whether the carrier treats cyber as a static product or as a living risk informed by loss data, claims experience, and resilience outcomes.

Below is the profile of a “good” cyber insurance carrier in the current ecosystem.

Realistic, Evidence-Based Underwriting

A strong cyber insurance carrier does not underwrite in isolation. Instead, underwriting decisions are continuously informed by live claims data, emerging threat patterns, and observed failure points across industries.

Rather than relying solely on theoretical models, good carriers decide limits, sublimits, conditions, and wordings based on how losses actually materialize.

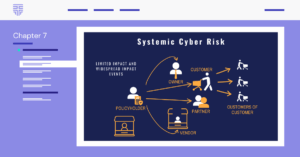

Business interruption, data restoration, outsourced IT failures, systemic events, and war-related ambiguity are addressed with clarity, reflecting operational reality, not optimistic assumptions. This alignment between underwriting and claims reduces coverage disputes, improves predictability for brokers, and ensures policies perform when insureds need them most.

Well-Designed Policies

For insureds and brokers alike, the quality of a cyber insurance carrier is immediately visible in the structure of its policy.

Good carriers design policies to work under stress. Coverage grants are clear, exclusions are transparent, and gray areas are minimized rather than hidden behind legal complexity.

Key exposure areas such as systemic risk, business interruption triggers, outsourced providers, and data privacy liabilities are addressed in ways that reflect how organizations actually suffer loss, not how policies are easiest to draft.

Investment in Resilience

The strongest cyber insurance carriers recognize that insurance is not just a balance sheet transfer; it is a resilience strategy.

Good carriers pair limits with meaningful, practical services that reduce both frequency and severity of claims.

These may include data mapping, privacy and risk assessments, tabletop exercises, vulnerability management, incident response planning, retainers, and sector-specific guidance. A carrier that invests in resilience improves outcomes not just for the insured, but for the entire portfolio.

Claims Partners Rather Than Gatekeepers

The true test of a cyber insurance carrier is revealed during an incident.

A good carrier shows up to claims as a partner. Claims teams move quickly, connect insureds with vetted vendors around the clock, and focus first on containment and recovery.

Critically, the structure of the claims team matters. Most cyber claims are operational before they are legal. Speed, containment, and decision-making reduce downstream legal exposure and overall loss severity.

Experience compounds this advantage. Carriers handling thousands of claims annually build institutional memory, regional fluency, and pattern recognition that cannot be replicated on paper.

Brokers and Policyholder Education

One of the most overlooked traits of a good cyber insurance carrier is its commitment to education. Great carriers actively educate brokers and insureds on coverage intent, claims mechanics, complementary services, and realistic loss scenarios. They provide guidance on what to expect during a claim, how timelines work, which vendors are involved, and how insureds can reduce friction during recovery.

This education reduces misunderstandings, improves claims efficiency, and elevates the overall quality of cyber risk conversations across the market.

Raising the Bar for Cyber Insurance Carriers

A good cyber insurance carrier is no longer defined by capacity alone. It is defined by how well underwriting, policy design, claims, services, and education are integrated into a single resilience strategy.

Carriers that align underwriting with reality, design policies for real loss, invest in resilience, show up as claims partners, and educate the ecosystem are shaping a more sustainable cyber insurance market.

Understanding how to evaluate carriers, claims models, and coverage intent is a learned skill.

The CCIS course is designed to build coverage literacy, claims awareness, and market insight that underwriters need to distinguish between cyber policies that look good and those that actually work.

→ Explore the CCIS course and learn how educated cyber underwriters are raising the standard