This month, Cisco announced the End of Life (EOL) for its flagship vulnerability management product, Kenna (officially known as Cisco Vulnerability Management).

At first glance, this might appear to be a routine product sunset. In reality, it marks a fundamental shift in how cyber risk is assessed, measured, and insured.

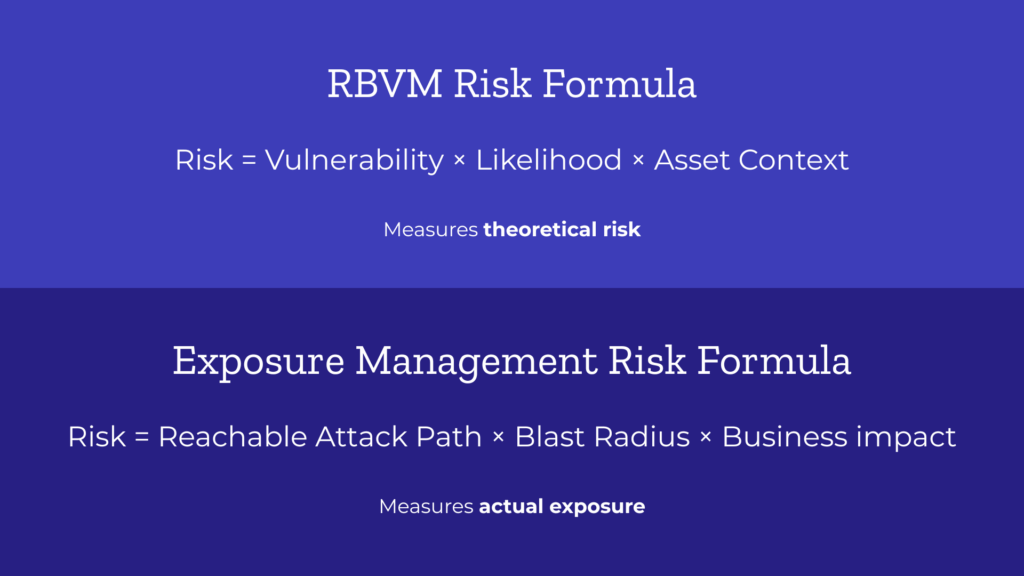

For insurance brokers, underwriters, and claims handlers, the retirement of a pioneer like Kenna is a signal that the industry is moving beyond Risk-Based Vulnerability Management (RBVM) toward a more holistic framework: Exposure Management.

What was RBVM and Why Did it Matter?

RBVM (Risk-Based Vulnerability Management) was designed to solve a specific problem: “vulnerability fatigue.” Organizations were overwhelmed by endless lists of software flaws.

The philosophy behind RBVM was that not every software vulnerability represents the same level of risk. Instead of patching everything, companies used tools like Kenna to prioritize fixes based on:

-

Threat intelligence and exploit availability.

-

Asset criticality.

-

Real-world context.

While RBVM was a massive step forward, it was built on a premise that is no longer entirely true: that an organization’s primary cyber risk sits within software vulnerabilities.

The Limits of the CVE: Why Software Flaws No Longer Define Risk

A CVE (Common Vulnerabilities and Exposures) is a standardized ID for a known software flaw. For years, CVEs were the primary entry point for attackers, making them the “North Star” for cyber insurance underwriting.

However, in modern, cloud-first environments, major incidents are increasingly bypassing software flaws entirely. Instead, they stem from:

- Compromised identities and credential theft.

- Excessive or “shadow” permissions.

- Cloud misconfigurations.

- Exposed API keys and “secrets” in code.

These are security vulnerabilities, but they are not software vulnerabilities. Because they do not have a CVE ID, traditional RBVM programs often fail to capture them.

From “Which CVE?” to “Which Attack Path?”

In today’s landscape, the question for an underwriter or broker is no longer “Which CVE is the most severe?” It must be: “Which combination of conditions creates a viable attack path with business impact?”

The Attack Path Comparison: Consider a medium-severity CVE on an isolated virtual machine. In an RBVM model, this is low priority. However, if that same machine is internet-facing and has “Identity and Access Management” (IAM) permissions to a sensitive database, it represents a critical exposure.

RBVM sees a single data point; Exposure Management sees the entire map an attacker would use to cause a claim-level event.

The Evolution of Cyber Risk

For years, the “cheese” in cybersecurity – the goal for defenders – was managing the CVE. RBVM helped organizations reach that cheese faster. But as infrastructure moved to the cloud, the cheese moved too. It now lives in the connections between systems and the permissions granted to users.

The Cisco Kenna EOL highlights that simply running toward where the cheese used to be is no longer a viable security strategy.

What This Means for Cyber Insurance Professionals

As the market shifts from vulnerability management to exposure management, insurance professionals must adapt their technical assessments:

1. For Cyber Insurance Brokers

It is no longer enough to ask a client how they score and patch software. To properly advocate for a client’s risk profile, you must ask how they manage non-CVE exposures, such as Identity and Access Management (IAM) and attack path modeling.

2. For Underwriters

Legacy scanning tools that only look for open ports and CVEs are becoming “noisy” but less predictive. Two applicants with the same RBVM maturity can have vastly different risk profiles based on their cloud configuration and “blast radius” controls.

3. For Claims Handlers

Understanding the shift to exposure management helps in post-incident analysis. Many modern claims do not originate from an unpatched server, but from a “cascading” event where a minor configuration error allowed an attacker to move laterally through an entire network.

Stay Ahead of the Cyber Risk Curve

The transition from Kenna and traditional RBVM to modern exposure management is just the beginning of a broader evolution in cyber risk. Understanding these shifts is critical for providing expert advice and maintaining a profitable book of business.

Want more insights into how evolving technology impacts cyber insurance policies?

Sign up for the Cyber Insurance Academy Newsletter to receive monthly updates on EOL announcements, emerging threats, and the latest in cyber underwriting trends.